下载掌阅APP,畅读海量书库

立即打开

On 21st Jul.2005 China announced that its currency RMB no longer be pegged to the U.S.dollar

.A gradual reform on exchange rate regime has been implemented in order to absorb external shocks and maintain policy authority.China then launched a managed exchange rate regime and planned to transit towards greater exchange rate flexibility step by step.

.A gradual reform on exchange rate regime has been implemented in order to absorb external shocks and maintain policy authority.China then launched a managed exchange rate regime and planned to transit towards greater exchange rate flexibility step by step.

From 2005 onwards,China's exchange rate regime has been evolving in a smooth way to a more flexible exchange rate arrangement.So far,China has gone through the following five distinct regimes regarding its exchange rate regime reform.

After two decades' economic reform,pegged currency arrangement was found not helping China's economic growth any more.It became unsustainable and undesirable for responding to realside shocks as well as to secular changes in the economy such as real appreciation.China moved into a managed floating exchange rate regime based on market supply and demand with reference to a basket of currencies.To increase exchange rate flexibility over time,a daily rate of Chinese yuan against a basket of currencies was announced before the start of the trading day.This rate acted as an anchor to form the midpoint of the band within which the USD/CNY rate

could fluctuate on that day.The previous day's close was applied as the central parity.A daily band of 0.3% around this central parity was allowed for USD/CNY rate.Other foreign currencies against Chinese yuan were granted an extra 1.5% fluctuation comparing with USD/CNY rate.The People's Bank of China as the central bank,would make adjustment of the exchange rate band when necessary according to market development as well as the economic and financial situation.

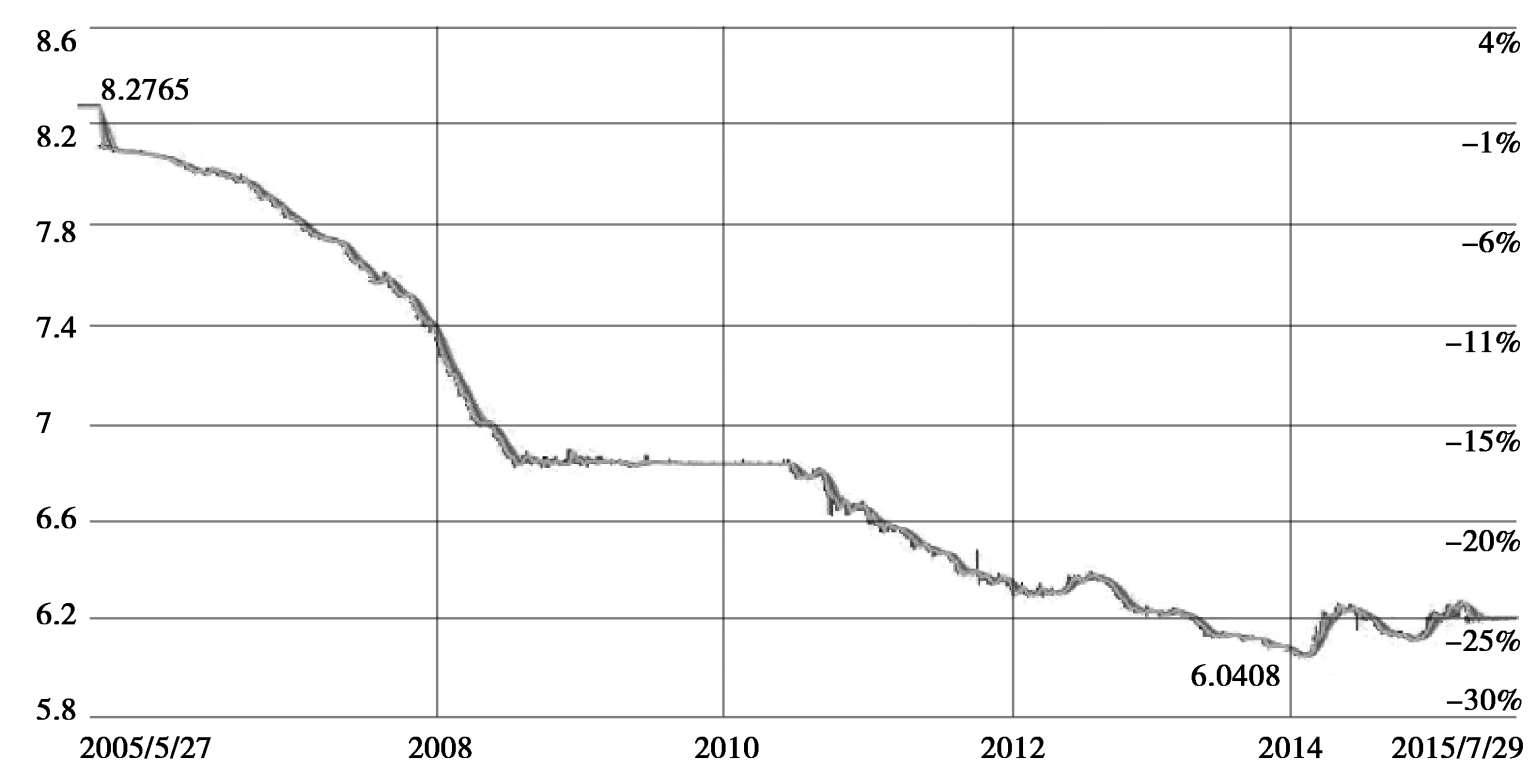

The Jul.2005 reform was accompanied by a 2.1% step revaluation of Chinese yuan.As one can find from Figure 1-3 below,the Chinese yuan was managed to appreciate gradually against the U.S.dollar,except for during the global financial crises when the rate was kept fixed again at around 6.8 yuan per dollar.

Figure 1-3 Managed Appreciation of Chinese yuan against U.S.dollar

As stated by the People's Bank of China,the central parity and band mechanism have been adjusted consistently.In May 2007,for example,daily band of USD/CNY has be released to 0.5%.Then the formation of central parity has been changed.Before the opening of the market on each business day,all market makers report their prices to China Foreign Exchange Trading System(CFETS).The highest and lowest offers being excluded,and then the weighted average of the remaining prices in the sample is the central parity of USD/CNY for the day.

Markets for forward,swap and option have been established during that period of time.With reserves increasing from 733 billion dollars in Jul.2005 to 3.99 trillion dollars in Jun.2014,China was able to moderate its currency appreciation from Jul.2005 to Jul.2015(appreciated by 26%against U.S.dollar).

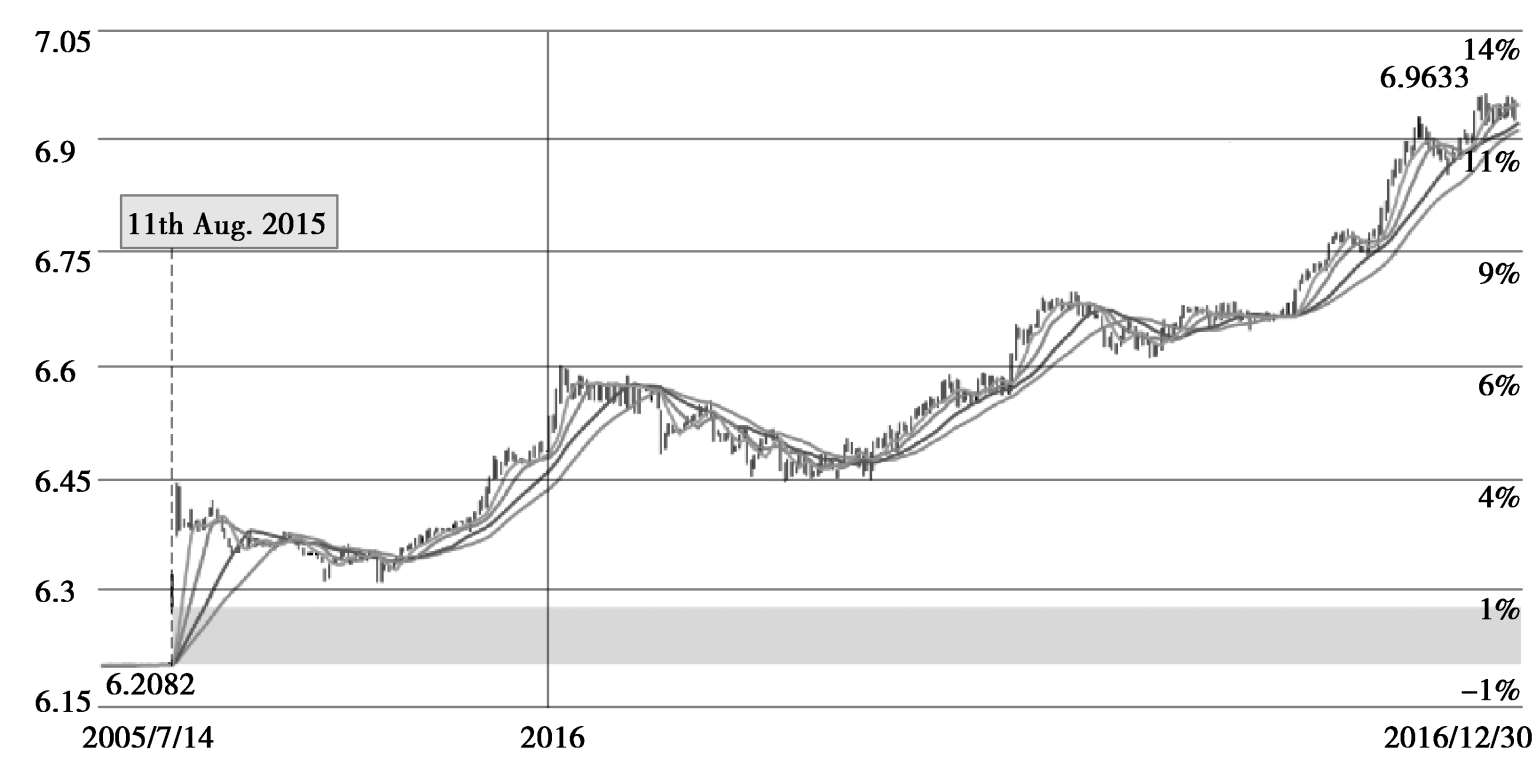

On 11th Aug.2015,central parity quoting mechanism was amended accompanied by a depreciation of Chinese yuan as shown in Figure 1-4.Market makers in China's foreign exchange market offer their prices referring to the closing rate of the inter-bank foreign exchange market on the previous day and in conjunction with demand and supply condition in the foreign exchange market and exchange rate movement of the major currencies.

Figure 1-4 Exchange Rate Performance Since Central Parity Quoting Mechanism Amended

This depreciation,plus unwinding of carry trades,and official foreign asset acquisition as well as some capital flight have accelerated a capital outflow.Foreign exchange intervention and moral suasion were employed to stabilize the exchange rate.Fluctuations of exchange rate serve to adjust trade and investment activities with multiple trading partners,the bilateral USD/CNY exchange rate alone is not enough to serve as a good indicator of the international parity of tradable goods.The China Foreign Exchange Trade System thus has published CFETS exchange rate index on its website on 11th Dec.2015.Market makers were instructed to both consider the CFETS currency basket and refer to the Bank for International Settlements(BIS)and Special Drawing Rights(SDR)baskets in a bid to remove the noise among the changes in the currency basket.

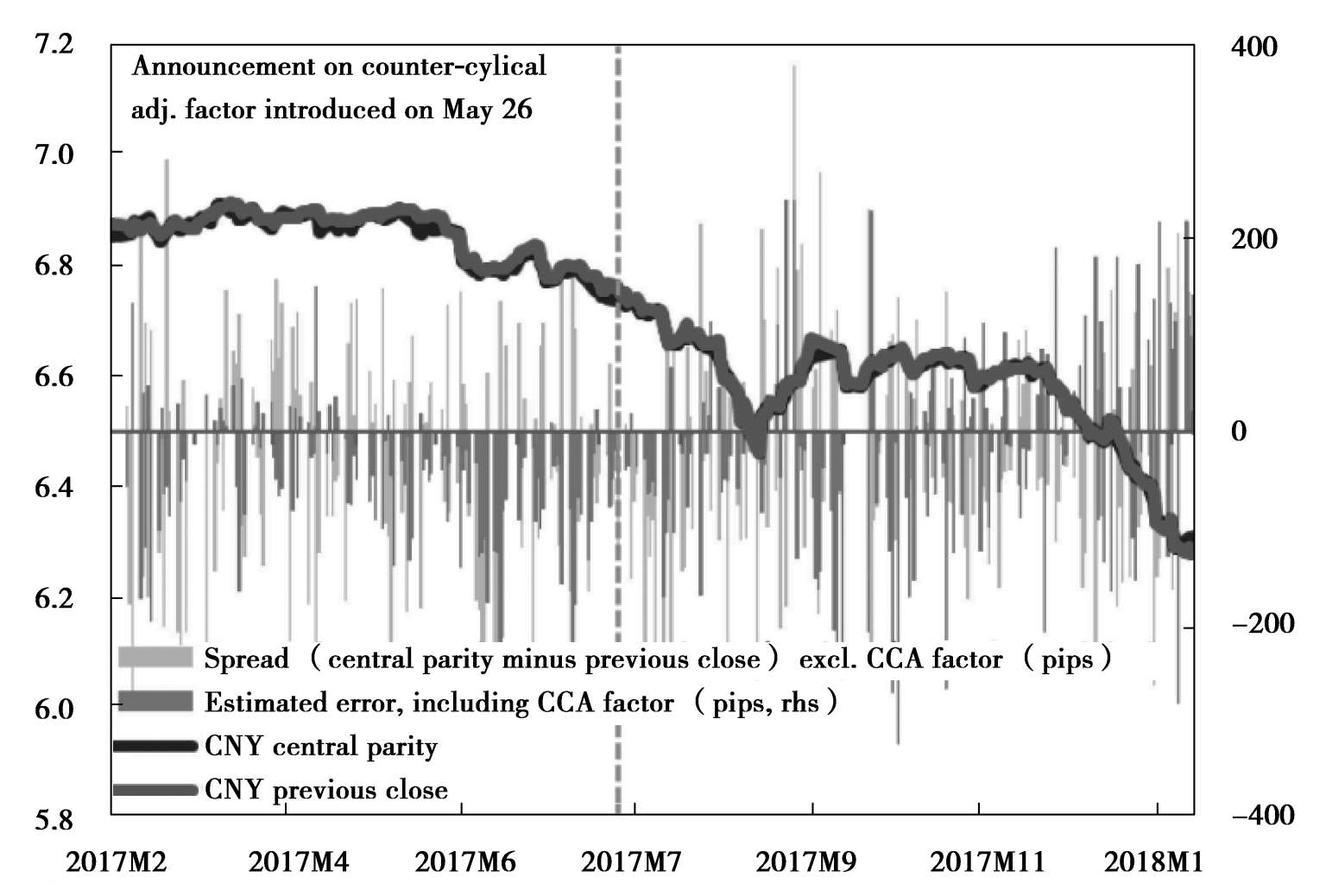

With capital flow management and foreign exchange intervention as well as guidance on the central parity mechanism,Chinese yuan has been stable against the CFETS basket during this period of time and foreign reserves began to increase in Feb.2017.The transition to an adjustable basket peg that was announced in 2005 has been accomplished.In order to curb irrational depreciation sentiment and pro-cyclical herding behavior,the CFETS had adjusted its guidance to market-making banks on their central parity quotes on 26th May 2017 by introducing countercyclical adjustment factor to the existing pricing model of the yuan's central parity rate against the U.S.dollar.Pass-through from the previous day's closing rate to the current day's USD/CNY central parity rate was reduced as shown in Figure 1-5.

Figure 1-5 USD/CNY Central Parity

Source:bloomberg and IMF staff estimations

Market-making banks during that period of time employed different parameters to reflect their assessment of economic fundamentals,and foreign exchange intervention played a more important role in exchange rate stabilization than the central parity mechanism did.

As capital flows were quenched,the counter-cyclical adjustment factor was then set to neutral but not dropped in early 2018.

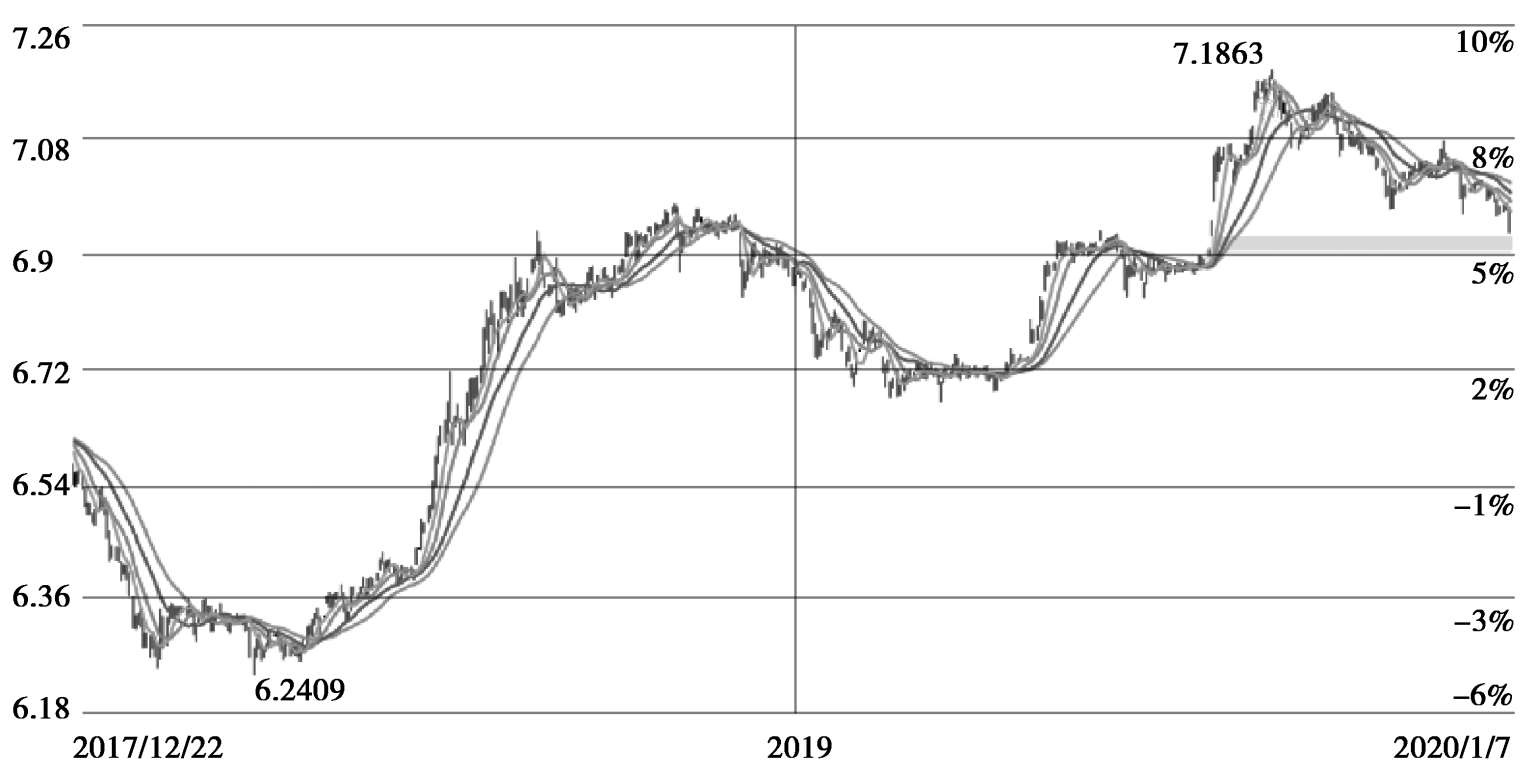

In the first half of 2018,progress towards a floating exchange rate was continued till the rising trade tensions and initial signs of slowdown in the economy across the world.A significant depreciation of Chinese yuan arose but the volatility was reduced by measures such as re-instituted the reserve requirement,re-activated the counter-cyclical adjustment factor and some indirect interventions.A continued gradual transition to a higher flexibility exchange rate was in progress till the world economy was hit by COVID-19.

Figure 1-6 A Transition to A Higher Rflexibility Exchange Rate

When China went under COVID-19 lockdown in Feb.2020,there was a massive short-term disruption to global supply chains.However,as the rest of the world went into lockdown in Mar.and Apr.2020,China swiftly resumed production.In fact,China emerged as a highly productive and reliable supplier for large quantities across a broad range of goods.

Robust economic recovery from the COVID-19 pandemic in China enhanced confidence further in Chinese yuan which remained generally stable.The pandemic has been effectively controlled and China's social and economic activities have been on a steady path of recovery since the second quarter of 2020.China eventually turned out to be the only major economy to have a positive GDP growth rate in year 2020.Positive prospects for China's exports and increased holding of CNY-denominated assets by overseas investors have led to a relatively mild appreciation of Chinese yuan,which was still in line with the performance of other major international currencies and also in line with China's goal of increased exchange rate flexibility.Shanghai's lockdown in April 2020 has led a dramatic depreciation,which has rallied back as the COVID-19 curb be lifted.

By Oct.2020 market-making banks have phased out the use of the counter-cyclical adjustment factor in the pricing mechanism of Chinese yuan's central parity rate against the U.S.dollar.They have made the move on their own initiative based on their judgment of economic fundamentals and market situations.The transparency and effectiveness of Chinese yuan's existing pricing model has been improved by this adjustment.Chinese yuan pricing is more market-based.

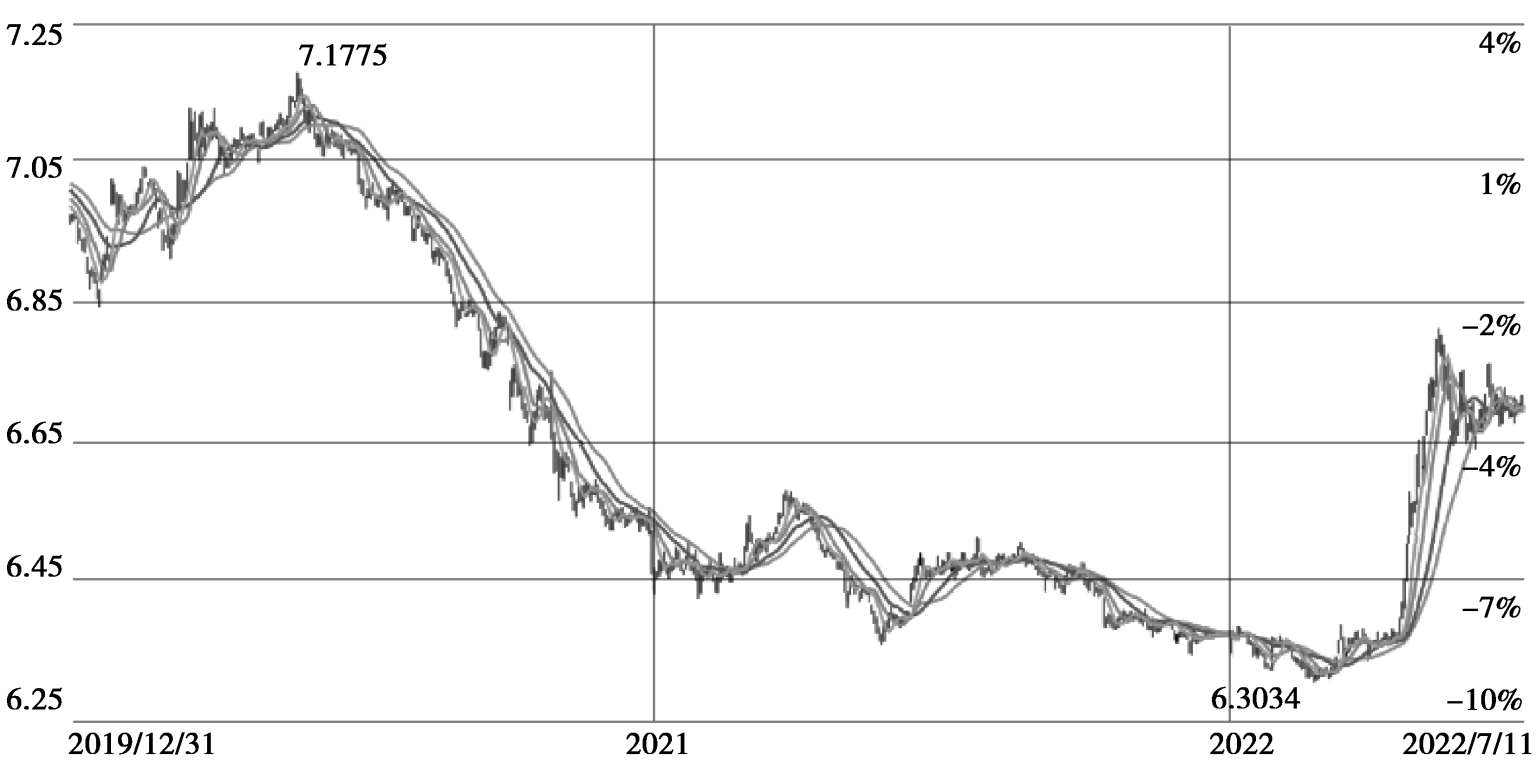

Figure 1-7 Exchange Rate Fluctuates with Economy Performance

Zero-COVID policy has kept service imports by Chinese tourists low and China's exports jumped to a record$325.5 billion in Nov.2021 and the current-account surplus in the first three quarters of year 2021 reached the equivalent of$203 billion,the highest since 2015,according to State Administration of Foreign Exchange data.With long-term goal of promoting more balanced two-way capital flows and maintaining the general stability of the Chinese yuan,the short-term appreciation momentum has been keenly supervised.The expanded Qualified Domestic Institutional Investor(QDII)quotas facilitated more outbound investment and helped balance the influx of money,thus easing pressure for Chinese yuan appreciation.

Before COVID-19,invoicing in CNY provided advantages such as hedging risk and advantages in price negotiations.CNY has evolved increasingly relevant to international settlement.A stable Chinese yuan encourages an even higher portion of CNY invoicing,which contributes to internationalization of Chinese yuan.Since the offshore RMB(Chinese yuan)market established in Hong Kong Special Administrative Region in 2010,other offshore centers have developed in several countries enhancing the degree of internationalization of China's financial sector.